To start the investment plan, you can divide your savings into a range of instruments providing varying levels of risk and returns

Some financial needs arrive unexpected. Their short-term nature means you have little time to plan for them. Generally, a financial goal that needs to be completed within a year is treated as a short-term one. It could be for buying a high-end motorcycle or taking a holiday trip with your family. It could even be making a small extension of your existing house. Whatever be the short-term goal, it can be scored with a strategic financial plan. You can either borrow for the goal, or save money yourself.

Let’s say you chose to go solo – you will save and invest to self-fund your goal. Since the investment tenure is as short as 12 months, it is recommended you pick a low-risk instrument that keeps your money safe, provides moderate to good returns, and can be easily liquidated.

Your investment options

Remember that before planning this goal you should factor in your essential expenditures and current outstanding loans and liabilities. To start the investment plan, you can divide your savings into a range of instruments providing varying levels of risk and returns.

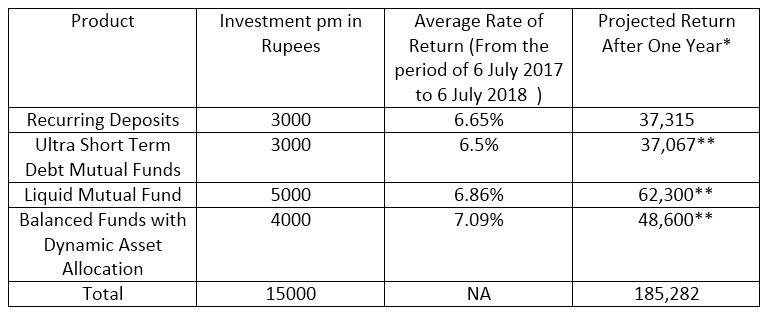

Let us take a scenario where you have Rs 15,000 per month to invest for the next 12 months (1 year). Here are the four types of investments you should consider to ease the process of meeting your financial goals.

a) Rs 3,000 in Recurring Deposits (RDs): RDs are nothing but term deposits which banks offer in which one can put a regular fixed monthly deposit and earn interest. You can allocate Rs 3,000 per month in an RD scheme for a year. Currently, the average prevailing interest rate for a 12 month RD is around 6.65 percent. At the tenure end, you should get a total sum of Rs 37,315. RDs generally attract Tax Deducted at Source (TDS) if interest income is above Rs 10,000. Since the interest here is not exceeding Rs 10,000, you do not have to pay any taxes.

b) Rs 3,000 in Ultra Short Term Debt Mutual Funds: Such mutual fund schemes help investors skip interest rate risks and have less than 50 basis points as expense fees with no exit loads. They primarily invest in liquid fixed income securities which have short-term maturities. Though these funds have their own, low degrees of risks, they tend to provide better returns than other money market schemes.

You can allocate Rs 3,000 per month to such a scheme. Currently, the category average return of Ultra Short-Term funds is around 6.5 percent. Since, you will be withdrawing the amount before three years, you will have to pay short-term capital gains (STCG) tax as per your income tax bracket on your debt investments.

c) Rs 5,000 in Liquid Mutual Fund: Debt mutual fund schemes primarily invest in money market instruments like commercial papers, treasury bills and certificate of deposits with low maturity period. They have lower than 30 basis points as expense fees and nil exit load.

These schemes are better alternative to savings deposits. You can allocate about Rs 5,000 per month in a liquid fund. Currently, the rate of return on liquid funds stands at 6.86 percent. Taking this into consideration the projected fund value at tenure-end should be about Rs 62,300. There will however, be a tax post redemption like any other debt fund.

d) Rs 4,000 in Balanced Funds with Dynamic Asset Allocation: Such mutual fund schemes tend to change their asset allocation on a daily basis in debt and equity. Generally, they can take their equity exposure to as high as 85 percent and as low as 30 percent depending on the market condition. The rest of the asset is allocated in debt instruments such as deposits, bonds and so on.

Compared with a pure equity or pure debt fund, dynamic balanced funds tend to do better and are relatively safe with low levels of interest rate and market risks as fund managers keep changing the ratio of asset allocation. For example, if the stock markets become overpriced, this fund may reduce its exposure to equity instruments and increase its debt. Likewise, when markets are weak, the fund increases its equity exposure and reduces debt. This way, investors get the maximum benefit of both the asset classes.

The last one year average return on such schemes stood at 7.09 percent. Taking this into consideration for future 12 months projections, the total amount one would receive would be somewhere around Rs 48,600.

Since such funds have the liberty to take the equity allocation to above 65 percent, they are considered as equity schemes and gains are accordingly taxed. Since gains are not in excess of Rs 1 lakh, you won’t be charged any LTCG tax. But make sure to redeem it after 12 months else you will liable to pay STCG tax of 15 percent.

*These figures are only indicative based on average return rates and do not depict any assured return.

** All figures are pre-tax. Tax will be applicable as per income slab of individual.

The above case is just an example of how you can achieve a short-term goal when planned correctly. Just remember to allocate disposable funds as per your appetite and refrain from allocating too much in order to avoid resorting to credit or breaking the funds midway for expenses.

The author is CEO at Bankbazaar.com

Original Source:

http://www.forbesindia.com/blog/finance/investment-options-to-pick-if-you-have-a-one-year-horizon/